Some First Republic employees could receive layoff notices within weeks as its new owner, JPMorgan Chase, takes stock of the bank’s operations in the wake of a recent takeover.

JPMorgan plans to notify First Republic employees within 30 days whether they will be offered a job at the bank, according to an internal email to staff sent May 11. Not everyone will be asked to join JPMorgan, the email said, and those who do will be offered either permanent roles or limited-term employment of between three months and 12 months.

First Republic staffers had been largely kept in the dark following JPMorgan’s takeover of the floundering regional bank, said a San Francisco-based employee who spoke anonymously citing potential job repercussions.

JPMorgan executives conducted a brief “town hall” meeting on May 2 following its buyout of the bank. On a shareholder call that day, JPMorgan Chase CEO Jamie Dimon said that the company would phase out the First Republic brand but seek to retain top talent at the bank, particularly in advisory services.

“The employees are having to do their own research,” said the First Republic employee. “Nobody feels like anything is guaranteed.”

JPMorgan said in the May 11 email it will provide notice, severance and access to transitional health benefits to First Republic employees who aren’t offered jobs and that staff will be notified of employment decisions by the first week of June. The bank declined to comment further on its plans.

Founded in 1985 in San Francisco, First Republic grew to become the third-largest bank in the Bay Area and the 14th-largest in the country before an unprecedented outflow of deposits in March pushed it to the brink of insolvency.

The bank’s customers withdrew about $100 billion from the bank’s balance sheet after the March 10 failure of Silicon Valley Bank (SVB) triggered a banking crisis. First Republic drew scrutiny for its seemingly similar client base—both banks catered to well-heeled customers who held deposits above the Federal Deposit Insurance Corporation’s $250,000 insurance limit—and for the low-cost loans it issued when interest rates were low.

In an April 24 earnings report, First Republic revealed the extent of its deposit losses and announced plans to lay off up to 25% of its workforce. In the subsequent days, the bank’s executives desperately sought to patch together a deal that would save it from a seizure by the FDIC, according to reports.

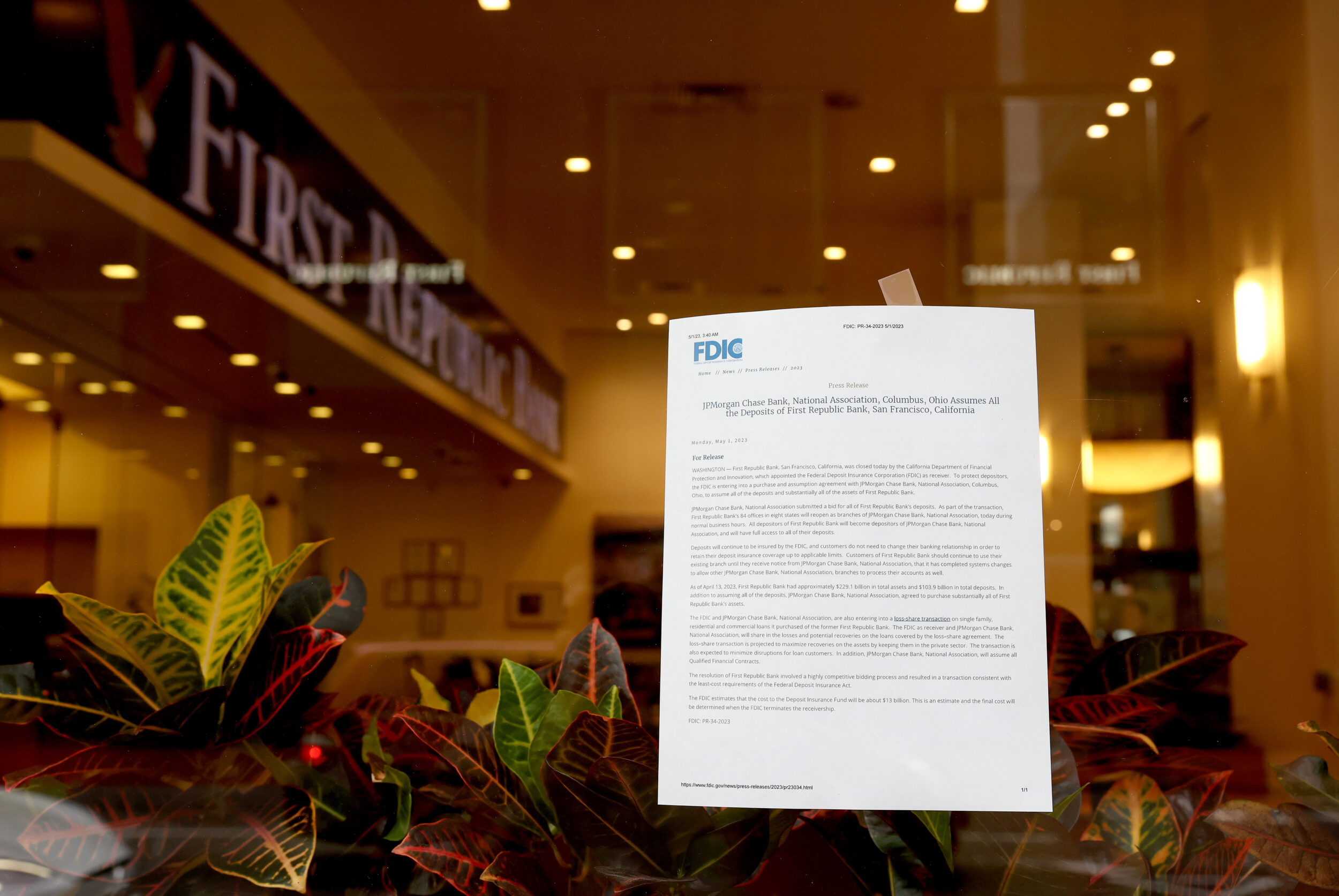

On May 1, federal regulators accepted a bid from JPMorgan Chase to take over First Republic’s assets of approximately $229.1 billion and total deposits of approximately $103.9 billion, along with 84 offices in eight states. The FDIC seized First Republic as part of the sale, making it the third major bank closure of the year following SVB and New York-based Signature Bank, which closed within two days of each other in March.

SVB—which was the 16th-largest bank in the country before its collapse—was placed under the control of a bridge bank for about two weeks before it was sold to North Carolina-based First Citizens Bank. A number of managers and other key employees serving the technology and venture capital sectors have taken jobs at other financial institutions, despite First Citizens’ assurances that it would continue to serve the region’s innovation economy.

First Republic employees who spoke with The Standard cited mixed emotions over the bank’s failure, saying that management might have better prepared for rising interest rates but contending that the bank would have survived if SVB’s failure hadn’t kicked off a banking panic. Several described it as a good employer but noted feelings of anger and disappointment among employees who had compensation tied up in the company’s stock.

First Republic had 7,213 employees at the end of last year, many of whom are based in the Bay Area. More than 40% of its total deposits originated in the Bay Area.

Meanwhile, First Republic customers received letters from JPMorgan Chase last week informing them that they should continue to use their usual branches for banking. The letter said that customers will eventually get access to JPMorgan’s services as First Republic is integrated into its operations.

When First Republic Bank failed on May 1st, JP Morgan Chase assumed all of its deposits. Depositors of the former First Republic must verify ownership of their funds by November 1, 2024. It’s super easy...just do one of these four things: https://t.co/4OHjlT9oRA

— FDIC (@FDICgov) May 15, 2023

First Republic customers were also advised that they must verify ownership of their funds with the bank by Nov. 1, 2024. That can be done by making a deposit or withdrawal from an account or taking a number of other simple actions, according to a statement by the FDIC.

The bank also cautioned customers against scammers pretending to be representatives of First Republic or JPMorgan.

"Very importantly, you should not respond to calls or texts claiming to be from JPMorgan Chase or First Republic that ask for your personal financial information," JPMorgan said in a statement.