The 1915 three-bedroom craftsman bungalow on Alameda’s west end was showing its age when Evan Phillippe and his wife bought it in late 2008 for less than the asking price. It was just weeks after the housing bubble had burst spectacularly. “We rolled the dice and got damn lucky,” said Phillippe. “And I’ve stayed here ever since.”

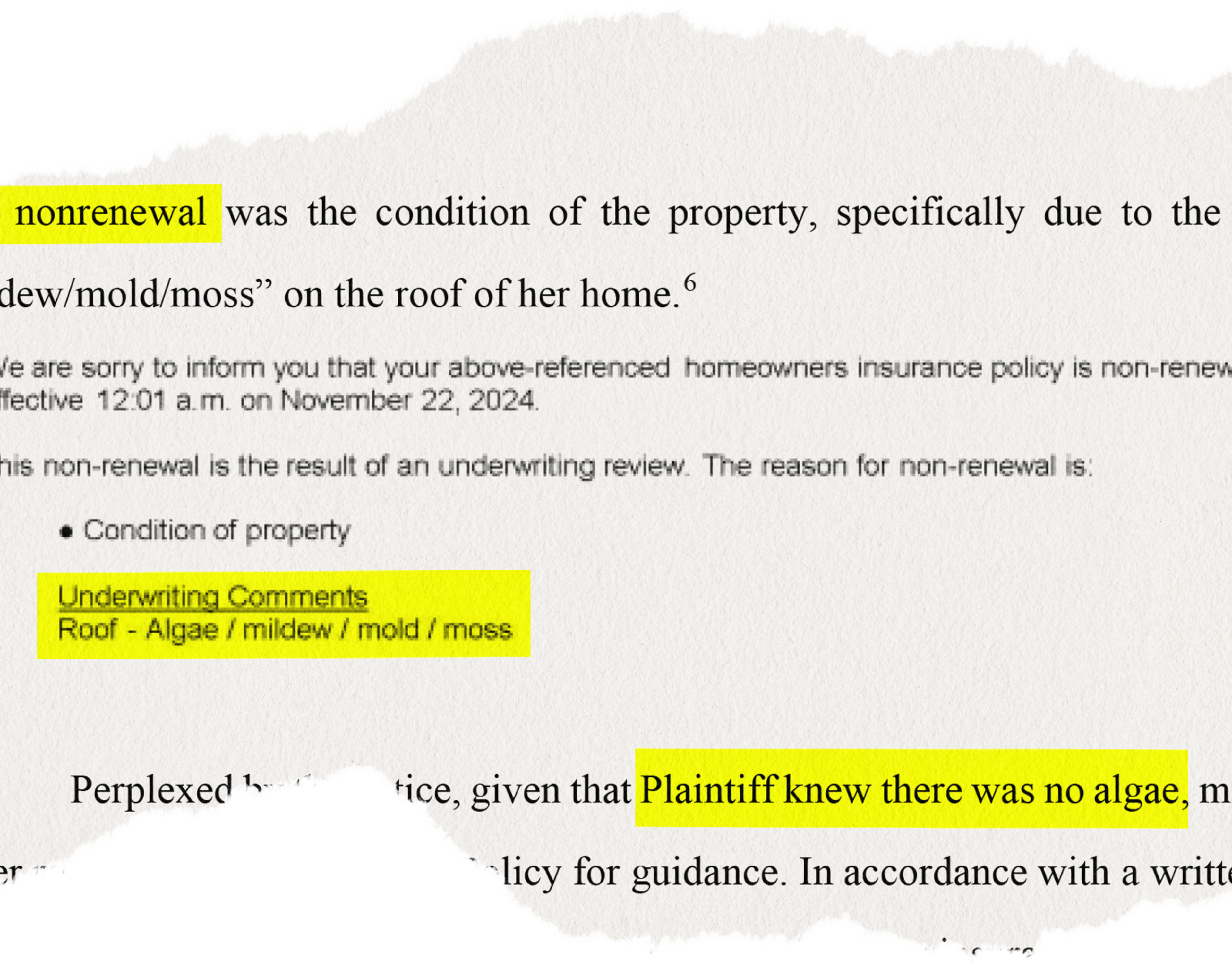

The yard was overgrown; the carpets were untacked and pulled back. But the roof was still in fighting shape. Phillippe got a close look at it every year when he ambled up a ladder to hang the holiday lights. So he was surprised when a curt letter arrived this fall from Liberty Mutual, the company that had insured the house for 16 years, citing “algae/mildew/mold/moss.” Just like that, effective February, Phillippe’s home would be uninsured.

Phillippe’s is one of at least 2.8 million policies that were not renewed in California over the last few years, according to the Department of Insurance. Insurers that are dumping their liability load in the state claim that regulations make it too expensive for them to operate and too difficult to raise rates.

Residents of the fire-prone wildlands and new buyers have borne the brunt of the crisis. But existing policyholders in ostensibly low-risk cities are also losing coverage — a loss enabled by emerging and unregulated technologies and data services, including aerial and satellite imagery.

That new tech is a mixed bag for consumers. It may feel violating to have your insurer fly a spy drone (opens in new tab) at low elevation over your backyard without your permission, but the pictures it snaps will at least be true to the condition of your house at that point in time (and, potentially, to your scantily clad self lounging by the pool). But when it comes to analysis of satellite and aerial images taken from thousands of feet up, the facts become blurred.

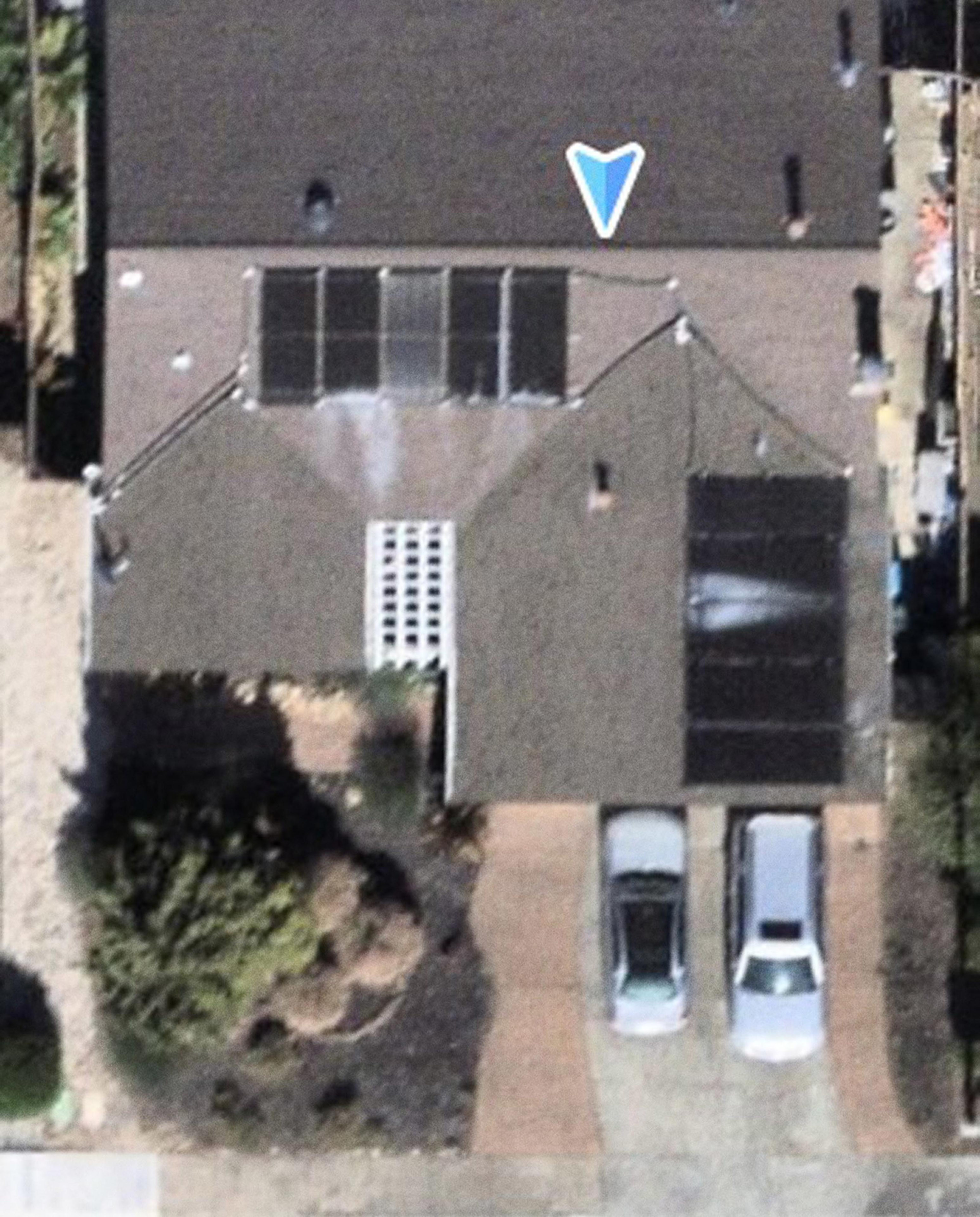

The Standard spoke with more than 25 homeowners who received nonrenewal notices like Phillippe’s, as well as realtors, inspectors, contractors, insurance brokers, and consumer advocates. From San Francisco to Novato, Pleasant Hill to East Palo Alto, Oakland to Santa Cruz, insurers are citing roof damage that does not exist, often with the supporting evidence of low-resolution imagery that highlights discolored pixels and shadows as policy-ending potential liabilities.

Subscribe to The Daily

Because “I saw a TikTok” doesn’t always cut it. Dozens of stories, daily.

“It’s an excuse, I think, very much,” said Phillippe, “so they can cancel as much as they can.”

And those cancellations can follow former policyholders for far longer than they might realize.

‘No mold here’

Alamedan Suzanne Arena’s letter cited an inspection, but there was no evidence that one had occurred. In Oakland, Karen Whittaker Crowe’s notice didn’t provide any details at all. The photo Sarah Burdick received in Santa Cruz wasn’t even of her own roof — it was her neighbor’s.

Liberty Mutual told Tim Beloney it had drone images of his roof damage. “And then the images that they sent were obviously far away, satellite images,” he said. The roof was less than 2 years old, but he spent $4,000 to resurface it, just to keep his policy.

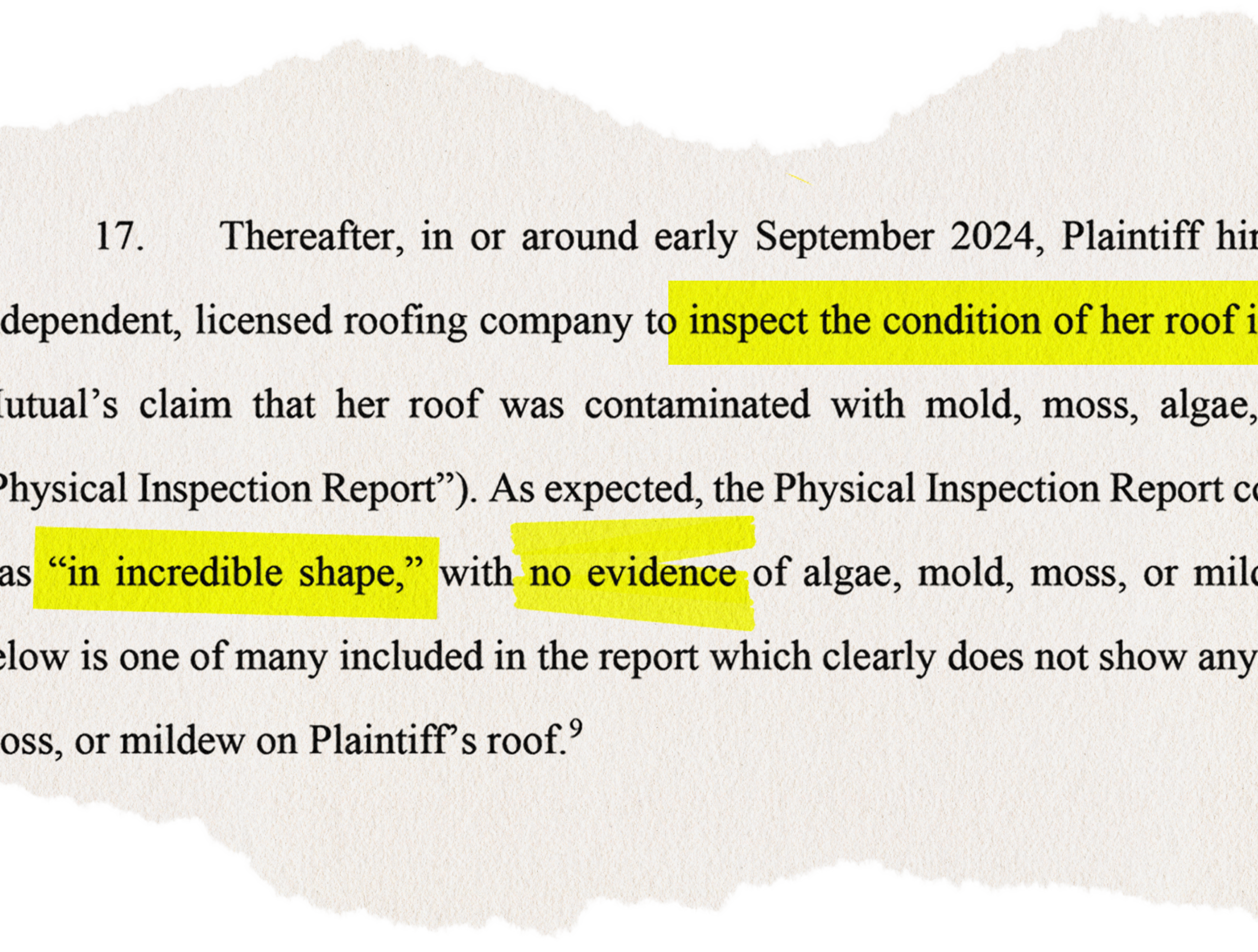

Adam Tow had four contractors inspect his roof after it was rated as “poor/major condition(s)” by Liberty Mutual. All found it to be in good shape, with no visible damage or growths.

A contractor told Ellen Ramirez her roof was fine for another five years, but she was so fearful of losing her insurance after receiving a nonrenewal notice that she replaced the entire thing.

This would be a gold rush for home inspector and roofing contractor Erast Dasari — if the money didn’t feel so dirty. “This is good for us in terms of, you know, the workload, but it’s very dishonest to the homeowners and insurance clients,” he said. “This is a complete scam. And I hate scams.”

Dasari both inspects and repairs roofs through his company Bay Area Home Inspections, which he said receives an average of one call a day from a homeowner who has received a nonrenewal notice. More often than not, Dasari finds their roofs to be in fine shape, but each inspection and report costs at least $685 — a small price to pay to keep a moderately priced longtime insurance policy, and far cheaper than a new roof, but an unexpected expense nonetheless.

“This is definitely not happening somewhere like Pacific Heights. We don’t get calls from them,” said Dasari. His bread-and-butter San Francisco neighborhoods are the Richmond, Sunset, downtown: “all the areas where the middle-class and poor people live.” He recently received an inquiry from an elderly woman in the Richmond with a decent roof and a letter from her insurer. “She was crying on the phone. Insurance straight up told her that you need the new roof. But it’s totally fine.” He did that inspection for free.

A report from Dasari or other certified contractors and inspectors has great sway, but there’s no guarantee that any evidence will convince an insurer to reconsider its roof judgment. The available recourse for homeowners is not always clear. Kira Harvath’s Safeco broker advised her to take photos of her roof repairs. “How am I supposed to provide you with proof that I’ve removed mold or algae when there was no mold or algae that ever existed?” Harvath countered.

For those intent on fighting back, licensed drone photographer Anne Kohler offers an alternative service. This fall, she zipped her camera back and forth at low elevation across the roof of Edward Barbera and his wife, who’d just been dropped by their insurance company. As her first clients, Kohler offered them a discounted rate of $200. “I’m not charging a lot of money to do this, because I feel sorry for the people going through it,” she said.

Once she’d sent off the photos, the couple’s broker responded within the hour to reinstate the policy.

Barbera ran inside and came back with a bonus for Kohler in the form of a bottle. “You drink Champagne?”

‘It’s really a Wild West’

A solid, modern roof is the key to surviving most of California’s climate chaos — wildfires and storms alike. It is also the element of a home that’s most exposed to aerial scrutiny. In just the past few years, companies catering to insurers have developed new tools and techniques to target roofs for closer evaluation.

LexisNexis launched its signature roof risk product (opens in new tab), which pairs aerial imagery and other publicly available data, including city permitting information. Its promotional materials cite escalating roof claims and repair costs, along with more extreme storms due to climate change. Eagleview, Verisk, and other companies specialize in the collection of aerial imagery and data for the insurance industry.

“It’s important to fully understand the condition of a property, and advances in aerial imagery are useful to identify issues that we — and homeowners — otherwise may not know exist,” a representative of Liberty Mutual and its Safeco division said in a statement. “Home maintenance remains very important.” The company contends that it does not use automation to make underwriting decisions and that a human reviews each case individually.

Use of this kind of aerial imagery is rising across the country. But in other states, regulators are stepping up to protect consumers against frivolous nonrenewals. The Pennsylvania Department of Insurance warned companies there (opens in new tab) that they had an obligation to conduct real-life inspections of roofs flagged in photos.

Amy Bach, executive director of United Policyholders, a nonprofit advocate for consumers, began drafting a state legislative proposal (opens in new tab) a year ago, when she first heard about the uptick in insurers using aerial photos as a basis for nonrenewal. That proposal recommends sharing photos with policyholders; detailing the precise liability, beyond a vague drop-down menu item; and creating a pathway to challenge the decision. So far no state legislators have taken it up.

“This tech thing is really a very slippery slope for homeowners,” said Bach. “We really don’t have rules in place to protect the consumer.”

That leaves homeowners to muddle through on their own, turning to NextDoor and neighborhood Reddit and Facebook groups for advice and commiseration.

“It’s really a Wild West when it comes to this aerial imagery, and we desperately need action by the insurance commissioner to rein in companies’ practices,” said Consumer Watchdog Executive Director Carmen Balber. “The tools are not regulated. The notices to consumers are not regulated. The nonexistent right of appeal isn’t regulated, because it doesn’t exist. There is no oversight of this practice.”

While new technologies have provided an immense amount of data for insurance companies to draw upon in order to make underwriting and premium rate-setting decisions, they have not made those decisions any better, said Balber. “The technology that companies are using is all over the map and frequently inaccurate.”

‘It becomes a massive problem’

For Evan Phillippe, the nonrenewal was a temporary inconvenience. Instead of fighting to keep coverage with an insurer that had turned on him, he sought out a new one. “If I wasn’t able to land something, I would have tried to fight it. I would have said, ‘I’ve got pictures; I know my roof is in good shape,’” he said. “I have a feeling that they might have repealed it, but who knows?”

Instead, he got lucky, landing a new policy with another company at the same rate — at least for a year. After that, as Phillippe said, who knows?

“What the public doesn’t generally understand is, once you get an adverse underwriting risk decision, the other insurance carriers know about it,” said attorney Michelle Meyers of Singleton Schreiber (opens in new tab). Much like a bad credit score, these nonrenewals have suddenly imperiled some homeowners’ loans. “You can also be adversely affected by your mortgage holder — your interest rate could change,” Meyers said.

Meyers represents San Diego homeowner Maria Badin, whose Liberty Mutual policy was not renewed over grainy aerial photos, with a notice identical to Phillippe’s. When Badin provided proof of roof quality, Liberty Mutual declined to reinstate her insurance. She filed a lawsuit in December, seeking class certification that could potentially apply to many more California homeowners.

“Obviously, insurance companies have the right to decide if they want to keep you as a client or not,” said Meyers. “The issue that I took with it is, don’t lie about it.”