In scripted calls Thursday morning, roughly 1,000 employees at First Republic Bank were informed that their services were no longer needed.

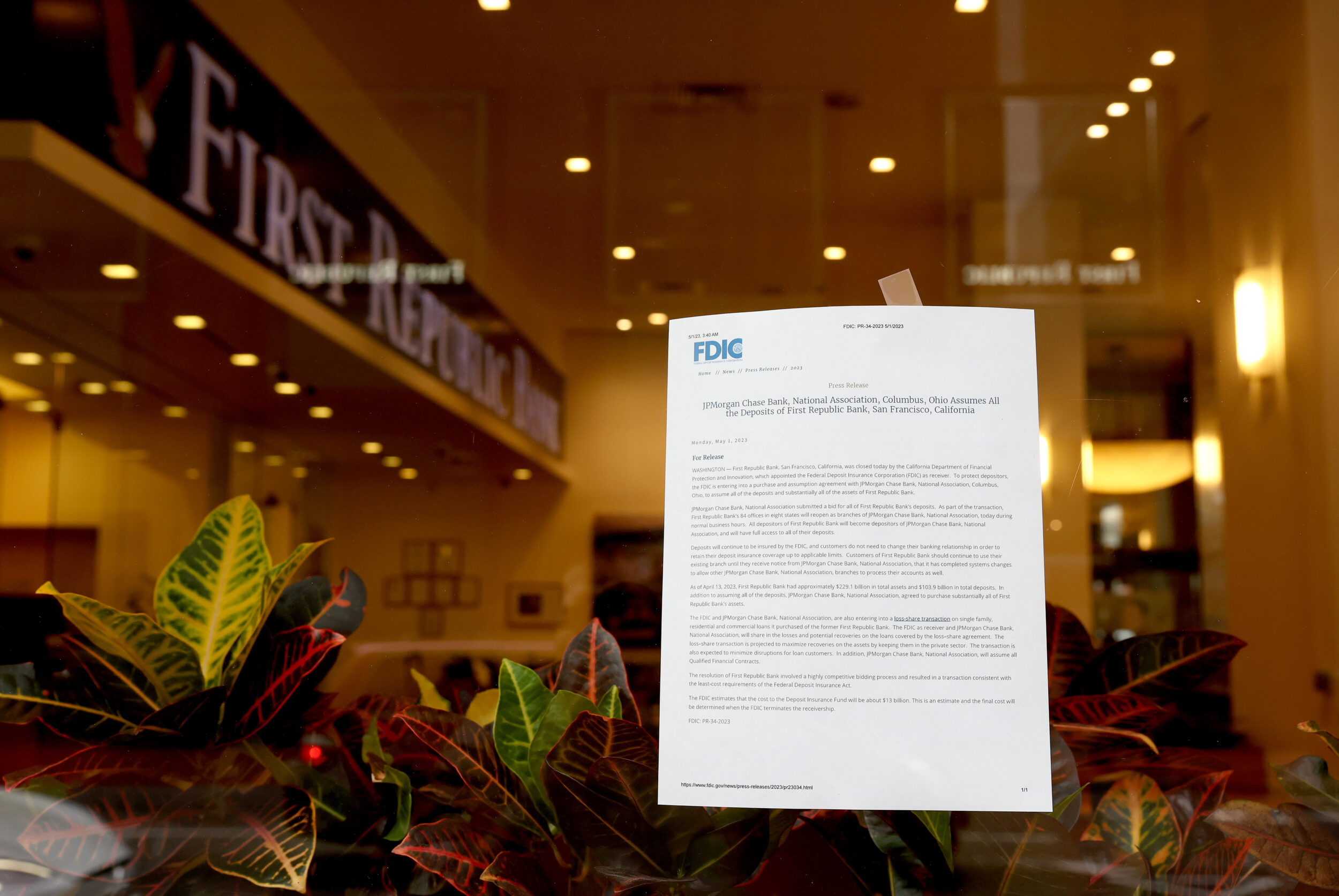

Job cuts were expected at First Republic, which was acquired by JPMorgan Chase May 1 in a deal that involved a government seizure of the San Francisco-based regional bank. First Republic employees were told in a May 11 email that some employees would be laid off within weeks, with others offered transitional roles of between three and 12 months or permanent positions with JPMorgan.

A JPMorgan spokesperson didn’t confirm the total number of employees who were laid off, but said that the company offered either transitional or full-time roles to “nearly 85%” of First Republic employees. The number of employees who did not receive an offer is fewer than the 20%-25% job cuts First Republic announced in an April earnings release, said the spokesperson.

San Francisco-based First Republic had 7,213 employees at the end of last year, according to its most recent annual filing, which would imply a layoff of roughly 1,000 employees on Thursday.

Are you a First Republic employee impacted by layoffs? Email us at tips@sfstandard.com. You can also call us at 415-408-6000 or send us a text message at 415-408-6282.

“The vast majority of First Republic employees will be offered employment at JPMorgan Chase—either through a transition period, or in many cases full-time,” the bank said through a spokesperson. “Employees who have not been offered a role will receive pay and benefits covering 60 days and will be offered a package that includes an additional lump sum payment and continuing benefits coverage.”

California’s Employment Development Department said it had not yet received any layoff notices from the banks.

‘Cutthroat’

Laid-off employees will receive regular pay through June 9 along with payments in lieu of the company’s 401K match, according to a recording of a layoff call obtained by The Standard. On or around June 13, they will receive a lump sum equivalent to 45 days of pay and are eligible for additional payments based on years of service, said a human resources employee who delivered the news.

A First Republic employee, who asked not to be named due to potential employment reprecussions, said laid-off employees received the news in brief calls during which a department head and a human resources employee read prepared scripts that gave no reason for the layoff.

Employees said that even high-level managers at First Republic were not privy to the specifics of the layoffs and were not included in discussions.

Throughout Thursday, laid-off First Republic employees gathered on a private discussion forum to commiserate and share information on how to access benefits. Employees who had paid family leave scheduled said they were unclear on whether they were entitled to company compensation for that period, writing that they had received no additional information from human resources that day.

“Everyone has been kept in the dark, even high-level managers are not being consulted,” the First Republic employee said, describing the layoff process as unceremonious and “cutthroat.”

Banking Chaos

The First Republic job cuts are the second major banking layoff this week in the Bay Area, with around 500 former employees of Silicon Valley Bank (SVB) getting pink slips from the bank’s new owner, First Citizens Bank, on Wednesday.

Laid-off SVB workers were told they would remain employees of First Citizens until June 9, with additional details about severance coming via email. According to one director-level employee, additional layoffs may be coming.

First Citizens snapped up SVB at a fire sale after the Santa Clara-based regional bank, which had served the Bay Area’s technology and investment sectors for decades, was abruptly shut down by regulators after a bank run drained $40 billion from its balance sheet in a matter of hours. Two days before it was placed under receivership, SVB had revealed in a filing that it had sold a trove of securities that had lost value as the Federal Reserve ratcheted up interest rates.

SVB’s failure kicked off a period of chaos in the banking sector as shareholders scrutinized other regional banks with high rates of deposits above the Federal Deposit Insurance Corporation’s $250,000 limit and liabilities on their books. Customers of First Republic, which served well-heeled customers likely to hold uninsured deposits, withdrew about $100 billion in March; JPMorgan Chase and a coalition of other banks deposited $30 billion into the bank in an attempt to shore up the floundering institution.

In an April 24 earnings release, First Republic announced a plan to lay off up to 25% of its workforce and other cost-cutting initiatives, but those efforts failed to reassure investors as the bank’s stock sunk to new lows: It closed at $3.51 per share the Friday before it was seized and sold to JPMorgan. Shareholders are expected to be wiped out in the deal.

First Republic employees described mixed emotions regarding the bank’s failure but noted anger and disappointment among employees who had significant compensation tied up in the company’s stock. In a statement to Congress this month, former First Republic CEO Michael J. Roffler said that First Republic was “contaminated overnight by the contagion that spread from the unprecedented failures of two regional banks,” referring to SVB and New York-based Signature Bank, which was also shuttered in March.

First Republic was founded in San Francisco by Jim Herbert in 1985 and grew to become the third-largest bank in the Bay Area and the 14th largest in the country at the end of last year. It catered to high-net-worth individuals, with roughly 40% of its deposits originating in the Bay Area, and was known for attractive mortgage rates and high-touch customer service, gaining a base of loyal customers and longtime employees.

Laid-off First Republic employees who spoke with The Standard described the abrupt layoffs, delivered in the form of scripted video calls lasting less than 10 minutes, as the culmination of a tense few weeks during which they received very little communication from JPMorgan.

“There was no respect; they treated us like a red-headed stepchild,” said one East Coast-based First Republic employee, who asked not to be named due to job repercussions.

Employees who are offered temporary roles with JPMorgan were told Thursday that they would receive details in a subsequent email. Employees have until June 7 to accept the offer, according to a recording obtained by The Standard. On or around June 1, employees who are offered temporary roles will receive information about the duration of their transition period.

Those who accept the temporary offers will earn their current rates of pay “unless otherwise communicated,” said a human resources staffer. Those who don’t accept the temporary roles are not be eligible for severance or other benefits, she said.

The East Coast-based employee likened the temporary offers from JPMorgan to “golden handcuffs.”

“It’s unnecessary to put anyone through that. At least with SVB, they just killed everyone right then and there,” the employee said. “I don’t understand why [JPMorgan] is dragging this out.”

Changing Customer Service

A major lender and employer in the Bay Area, First Republic was considered a cornerstone of the region’s real estate sector.

The bank offered low-rate mortgages to affluent clients and understood the nuances of Bay Area business, making it the lender of choice both for many individuals, startups and small businesses. It was also embedded in San Francisco’s pool of affordable housing, having offered a $100 million revolving credit facility to the San Francisco Housing Accelerator Fund, which assists nonprofits in acquiring and renovating low-income housing.

First Republic customers received letters from JPMorgan Chase earlier this month informing them that they should continue to use their usual branches for banking. First Republic customers will eventually get access to JPMorgan’s services, said the letter.

First Republic employees said that given limited communication from JPMorgan, people in client-facing roles had struggled to answer questions from customers beyond the bare minimum about what would happen with their accounts.

But there are signs that JPMorgan, the largest bank in the U.S., will be taking a much different approach to lending than First Republic.

JPMorgan has begun culling personal lines of credit, telling customers that they will no longer be offered when they come up for renewal, according to the Information. The bank does not offer personal lines of credit.

Real estate professionals believe that the failure of First Republic could have ripple effects in the Bay Area housing market as well. On a May 2 shareholder call, JPMorgan Chase CEO indicated that the days of low-cost mortgages were over.

“We’re not going to be putting a lot of cheap jumbo mortgage loans on our books,” Dimon said. “First Republic did a great job at service. But being in the low-cost lending business is not what JPMorgan does.”