As gale-force winds picked up this week around his home in Brentwood, the quiet neighborhood in the Westside of Los Angeles, Karl Susman had a bad feeling.

Now, as fires torch swaths of the city’s hillsides, Susman, the owner of an insurance agency, has evacuated to a relative’s house, where he’s been on the phone nonstop with clients steeling themselves to the possibility of untold loss.

“There’s so much that has been burned away … but I’ve been so busy, I don’t think it’s really sunk in yet,” Susman said Thursday of the handful of fires that remained uncontained in the L.A. area.

A full accounting of the damages won’t be clear for months, but the total could top that of the 2017 North Bay firestorm ($9 billion) and the 2018 Camp fire ($12.5 billion insured damages).

“This has at least the potential to be collectively the costliest wildfire disaster in American history,” UCLA climate scientist Daniel Swain said during a YouTube broadcast. “This is going to send the wildfire home insurance crisis in California into the stratosphere, if it weren’t there already.”

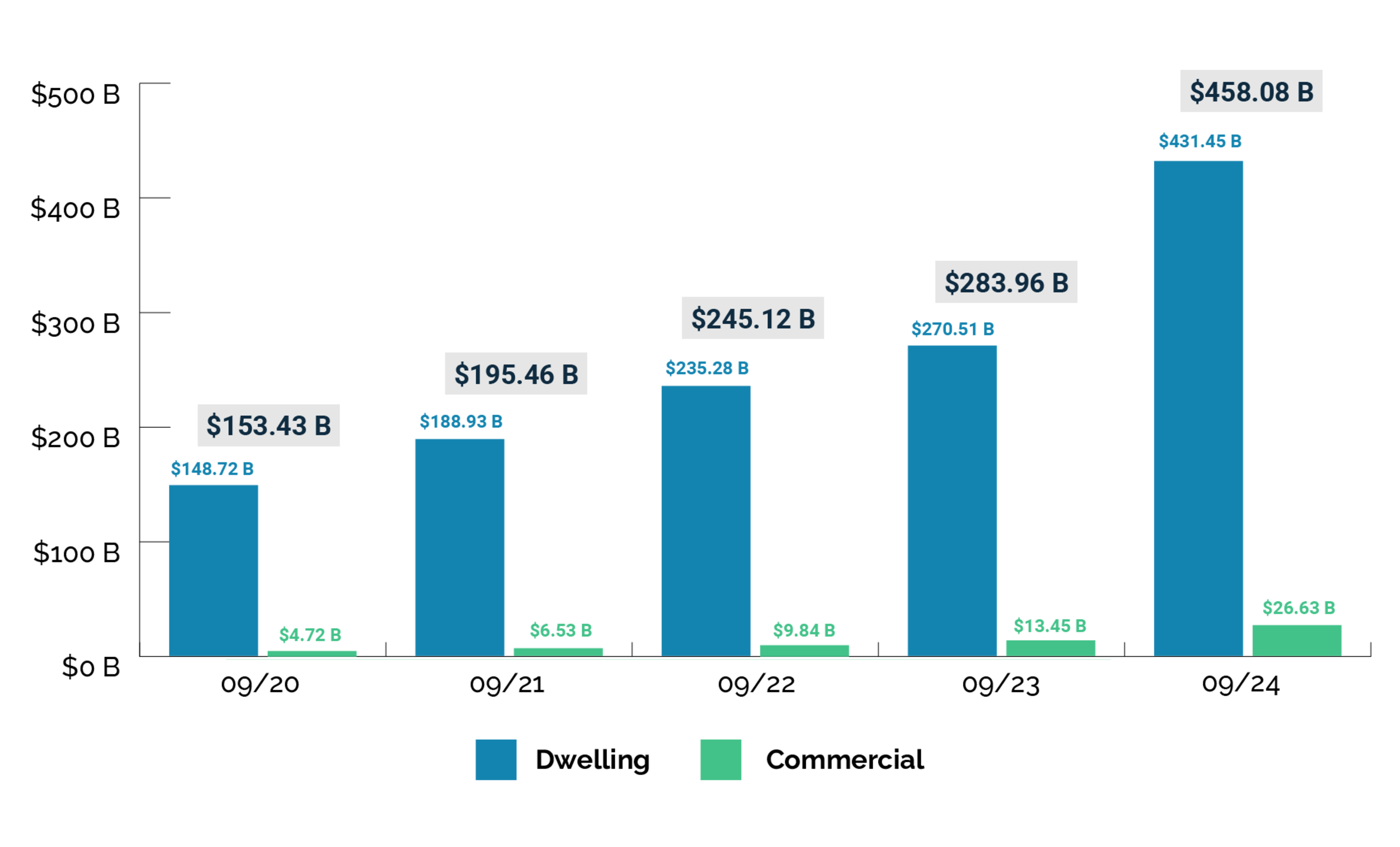

Potentially billions of dollars of those liabilities may be held by California’s FAIR Plan, the state’s home insurer of last resort. Every private carrier in the state is required to participate in the nonprofit plan, which was designed as a backup policy in the 1960s, an age of civil unrest and Southern California chaparral brush fires not unlike those burning this week. The FAIR Plan quickly became the only insurance option for homeowners in high-fire-risk areas across the state, and the number of policies remained stable for decades. But after the devastating 2017 and 2018 fire years, insurance companies started curtailing business, citing higher liabilities, and FAIR policy numbers ballooned.

In 2018, the FAIR Plan’s total risk exposure was $50 billion. By 2024, it had exploded to $458 billion. In Pacific Palisades alone, where the largest fire was still burning Friday, the FAIR Plan’s total liability is around $5.9 billion.

And under rules from the California insurance commissioner that were finalized this fall, that pain could be spread across the state in all new ways.

‘Batshit crazy conditions’

Last year, the tony beachside Pacific Palisades neighborhood became one of the places hit hardest by State Farm’s decision not to renew 72,000 home insurance policies across the state. The community experienced a nonrenewal rate of nearly 70%.

“This is exactly the situation that carriers have been afraid of,” Susman said. “The new climate environment we’re in nowadays means these types of batshit crazy conditions.”

Subscribe to The Daily

Because “I saw a TikTok” doesn’t always cut it. Dozens of stories, daily.

In many ways, the situation of Pacific Palisades mirrors the challenges of California’s insurance market in miniature, as homeowners flocked to the FAIR Plan, leaving it covering a high-risk population in an era of unprecedented climate catastrophe.

FAIR Plan growth is accelerating as private carriers have pulled back, according to the program’s latest data, with year-over-year policy coverage expansion topping 61% statewide. The number of FAIR Plan policyholders in Pacific Palisades increased by 85% over the same period.

Many of the ZIP Codes with the steepest upticks in FAIR Plan policy value over the last year are in San Francisco and the inner East Bay, in places not deemed at high risk of wildfire.

In San Francisco, the Twin Peaks area saw a 1,217% increase in residential policy coverage, and Portola saw a 674% jump. In the East Bay, the Bay Farm area of Alameda saw a 1,327% bump, and the east side of San Leandro was up 1,772%.

Berkeley tops the list of Northern California’s greatest municipal exposures under the FAIR Plan, with $5.5 billion in total liabilities. The East Bay hills enclave of Orinda saw the state’s largest number of nonrenewals from State Farm in 2024. There, FAIR liabilities stand at $4.2 billion.

At a March Assembly hearing in Sacramento, FAIR Plan President Victoria Roach painted the picture of a system on the brink — one catastrophic event away from insolvency.

Roach told the San Francisco Chronicle last year (opens in new tab) that the plan had about $385 million on hand to pay for wildfire damage to its policyholders. The plan also has funds available by bond and reinsurance that can backstop its financial position. But that may not be enough.

“As those numbers climb, our financial stability comes more into question,” Roach said of the FAIR Plan’s risk exposure.

‘Better anticipate future losses’

This fall, California Insurance Commissioner Ricardo Lara paved the way for a new kind of FAIR bailout.

Insurance carriers have long clamored for updates to regulations they claim artificially depress their rates and make it unprofitable to operate in California.

'Those people are looking at this situation and saying, this is supposed to happen one in 100 years, not three times in 10.'

Michael Wara, climate and energy policy program director, Stanford’s Woods Institute

They got their wish in the form of the Sustainable Insurance Strategy (opens in new tab), which was meant to get carriers writing new business in the state, particularly in fire-prone areas.

One new rule (opens in new tab) allows private insurers to cover the cost of large FAIR Plan losses by adding temporary supplemental fees to all their customers’ policies — up to half for liabilities under $1 billion, or the full amount above $1 billion. Of the 33 other states with a version of the FAIR Plan, only Florida and Louisiana allow insurance companies a similar worst-case bailout paid for directly by policyholders, with regulator approval.

That could mean a few hundred dollars levied on every premium bill, depending on the size of the gap.

“Given the degree of destruction we’re currently seeing, that’s very possible,” said Joel Laucher, a consumer advocate with the nonprofit United Policyholders.

Laucher, who worked for more than three decades as a regulator in the California Department of Insurance, cautioned that payouts from the current Southern California fires will likely take many months or even years to fully materialize.

The hope is that the FAIR Plan will be able to strengthen its financial position over that time, but only if no other catastrophic fire hits the state.

“Insurance coverage used to be a known thing you put in your budget,” Laucher said. “Now it’s become one major expense where you have no certainty of what it might be.”

The reinsurance that private carriers and the FAIR Plan rely on to offset their liabilities is in its annual renewal cycle.

“Those people are looking at this situation and saying, this is supposed to happen one in 100 years, not three times in 10,” said Michael Wara, director of the climate and energy policy program at Stanford’s Woods Institute and a consultant on wildfire and insurance policy.

If primary insurers can’t get reinsurance, they would have to keep more cash on hand to pay out potential claims — and could raise premiums accordingly. “We’re already in a situation where a lot of people are struggling to afford their homeowners insurance. But if things got 100% or 200% worse, then we’re in a different world,” Wara said.

Reinsurers would need “a clear signal that California takes this problem seriously,” he said, in order to head off another five years of escalating insurance crisis. “I think we are going to need confidence-raising measures taken to stabilize the situation.”

‘A big question mark’

The two other key provisions of Lara’s new rules allow carriers to use forward-looking wildfire catastrophe models to set rates, and give them the ability to pass the cost of reinsurance to policyholders.

Insurance companies are in the business of pricing and transferring risk, not reducing it, but the new rules do require the FAIR Plan to offer a discount to homeowners who reduce their risk with efforts such as installing heat-resistant glass and ember protection for eaves. New catastrophe models will also take landscape mitigation work into account when scoring risk and making underwriting decisions.

'Insurance is the canary in the coal mine when it comes to climate change. And the canary is almost dead.'

Dave Jones, former California insurance commissioner

But as for whether insurers will begin to write scores of new policies now that they are able to charge higher premiums, “that’s a big question mark,” said Dave Jones, Lara’s predecessor at the California Department of Insurance and the current director of UC Berkeley’s Climate Risk Initiative.

“This kind of event is why they sought the changes. They got the changes. They’re going to be filing for substantial rate increases, and they’re probably going to get them,” he said.

He expects the FAIR Plan policy load to continue to grow, along with the population for whom a FAIR Plan policy simply becomes too expensive to afford.

He would like to see government-funded insurance premium subsidies to help the less affluent afford homeownership.

Regardless, the system won’t capsize tomorrow, he said, even if the L.A. fires do add up to become the country’s most expensive disaster ever.

But he is pessimistic about the long term, as global temperatures continue to rise.

“Things may get better in the short and mid term because of these regulatory changes, but in the long run, we’re not going to ‘rate increase’ our way out of the climate crisis,” said Jones. “Insurance is the canary in the coal mine when it comes to climate change. And the canary is almost dead.”